The global agricultural market has been severely shaken by Covid-19. Palm oil is no exception, particularly in India, the world’s largest importer of the commodity.

Demand has fallen off a cliff in India since the prime minister, Narendra Modi, imposed a countrywide lockdown on 24 March to contain the pandemic. That has shuttered restaurants and hotels, major consumers of the oil.

Consumption of edible oil in India, which is dominated by palm oil, has crashed by nearly 40% since the national lockdown began. Palm oil imports may slump by as much as 25% in 2020, to the lowest levels in at least a decade, experts say.

Since 2001, palm oil – which barely figured in traditional cuisines – has gone from accounting for 29% of edible oil consumption, to nearly 65%. It blends well with other oils and suits frying, a key consideration in preparing Indian food.

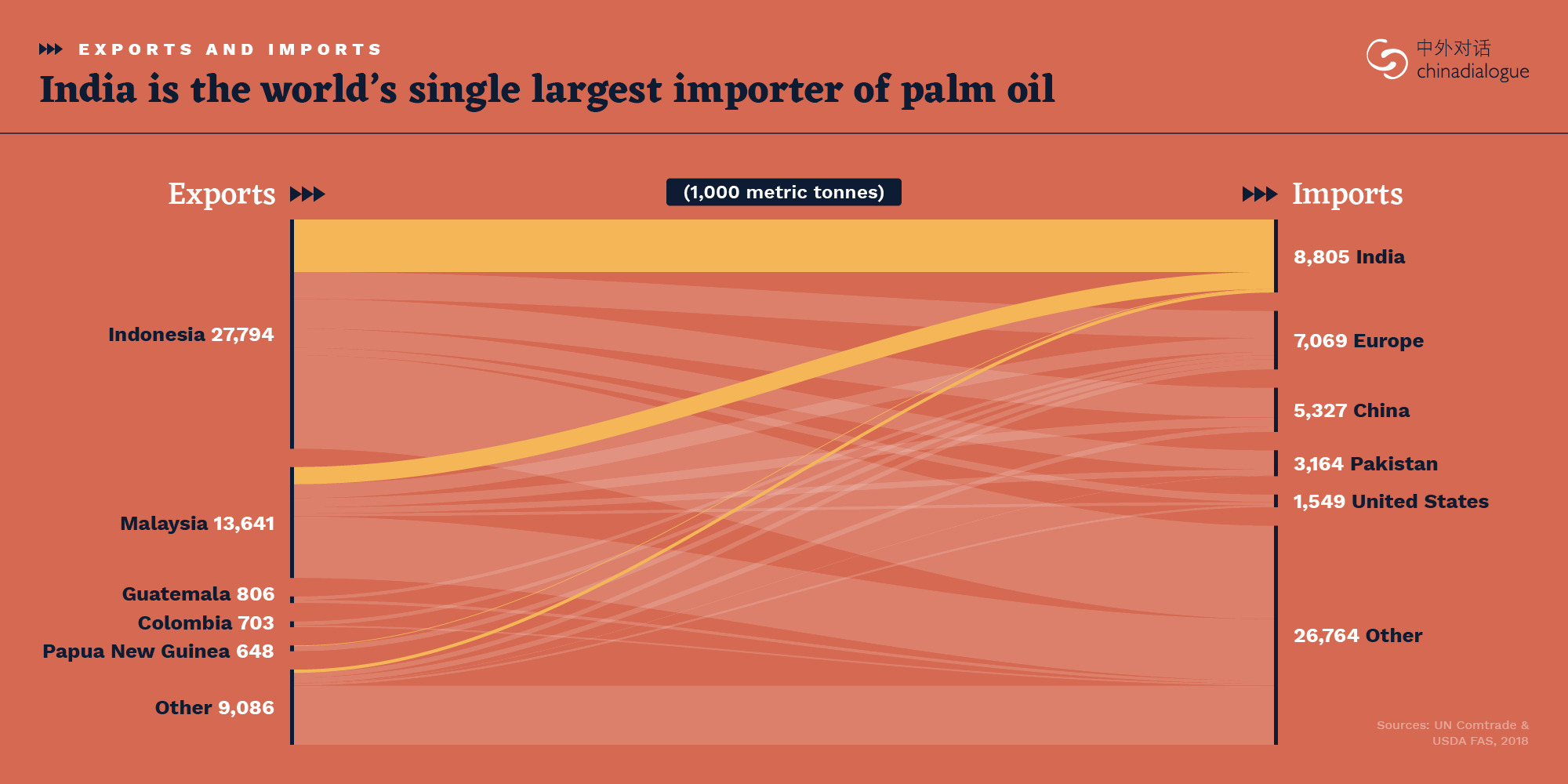

What happens to palm oil demand in India has a significant effect on the entire industry. Since India’s palm oil imports account for nearly 20% of the global trade, it has a big effect on efforts to make the production and processing of the commodity sustainable, ensuring that no further environmental damage is done.

The same is true for other major import markets such as China and the European Union, which account for 16% and 14% of the global trade respectively. In the EU, increased consumer awareness and government policies have brought about a turn towards sustainable palm oil in recent years. If such efforts can be replicated in India, it will go a long way to preserving rainforests in Southeast Asia.

Impact of demand

In little under three decades, India has become the biggest buyer of vegetable oils in the world. A rising urban population, changes in consumption patterns, and domestic production that has failed to keep up with demand, have contributed majorly to the country’s increasing importation of edible oils.

India’s palm oil imports rose at an average of 12% every year in the decade to 2015-16. It imports over 96% of the palm oil it consumes, primarily from Indonesia and Malaysia, the top two producers. As it well as its suitability for cooking, the country’s preference for palm oil has to do with its cheaper price compared with other vegetable oils and the proximity of production, meaning shorter shipping times.

At the same time, global production has been growing steadily in the past five decades. In the 20 years between 1995 and 2015, annual production quadrupled to meet demand, which is forecast to be between 120 and 156 million tonnes by 2050.

Already, palm oil plantations account for 10% of global cropland, according to the Center for International Forestry Research. The area of oil palm plantations has increased from 0.5 million hectares (ha) in 1985 to 20 million ha at present, according to World Rainforest Movement, a non-profit organisation. It is projected to reach 25 million ha by 2025.

10%

of global cropland is palm oil plantations

And the expansion of palm oil cultivation has driven deforestation to unprecedented rates. More than a third of large-scale oil palm expansion between 1990 and 2010 has contributed to significant forest cover loss in Indonesia, Malaysia and Papua New Guinea, WWF reports. Species including orangutans, the Sumatran tiger and Javan rhinoceros are on the verge of extinction due to a decrease in habitats as forests make way for plantations.

Every year, smoke haze blankets parts of Southeast Asia. It is generated by the deliberate burning of forests to clear land for plantations. In 2019 alone, close to 50 million people were directly affected by smoke caused by the clearing of forests for palm oil plantations.

This not only has severe implications for local people and ecology, but also for the global climate due to the sudden large release of carbon dioxide.

Value and supply chain

Currently, the majority of the import market in India is not driven by concerns linked to these environmental impacts. Research published in November 2018 shows that 58% of palm oil imports into India is not covered by NDPE policies: No Deforestation, No Peat, No Exploitation.

The import market is extremely price-sensitive in India, experts and industry insiders say. Importers are primarily looking at lowest price points for various grades of palm oil and are not yet overly concerned about how the commodity is produced. This is the primary barrier to the uptake of ethical palm oil in the country.

There are other obstacles to the increased use of sustainable palm oil, including the various unbranded vegetable oils sold in open market across the country, and the number of various grades of palm oil used in the supply chain.

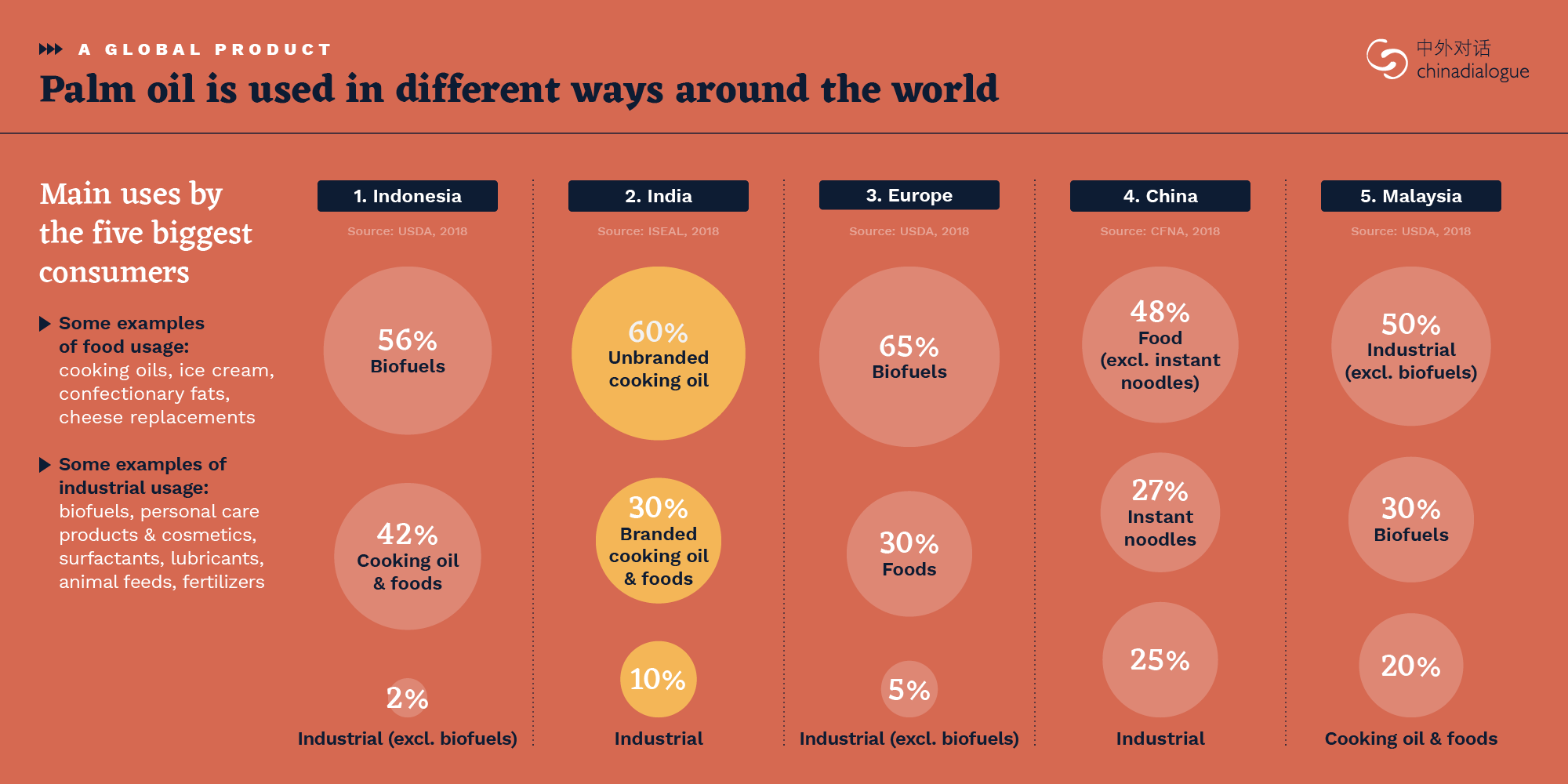

Unlike European and American markets, the market in India is mainly driven by large volumes in the food and cooking oil sectors (90%), with smaller volumes (10%) in consumer goods such as processed food and cosmetics. A significant proportion of Indian consumers buy so-called loose palm oil, without any brand association. Establishing a transparent supply trail becomes difficult in these conditions.

Palm oil for cooking is primarily used by commercial establishments, government procurement and in low to middle-income households. The government procures imported palm oil in bulk through its trading agencies for distribution and sale to lower income consumers at subsidised rates in the interest of food security during periods of price inflation. It is also distributed in some provinces as a food security measure for economically weaker sections of society.

Whenever there is serious price rise for cooking oil, the federal government intervenes by purchasing RBD (refined, bleached and deodorised) palm oil and crude palm oil through its trading agencies and distributes it to states with vulnerable populations. Since the lowest price at acceptable quality is the main consideration in this case, any addition to cost for sustainable oil takes a back seat.

Domestic production

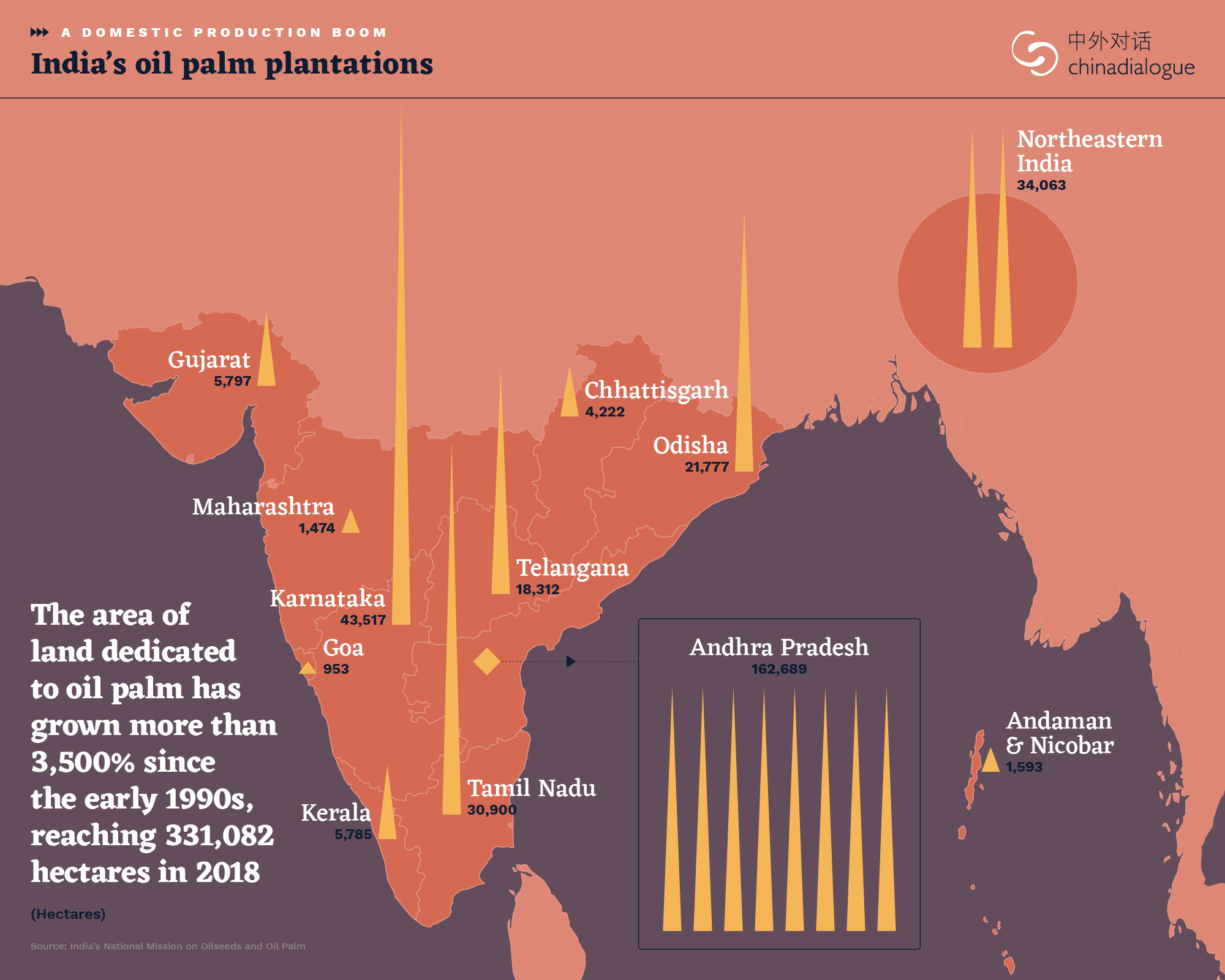

The widespread use of palm oil and reliance on imports have prompted the Indian government to devise schemes to promote domestic production by increasing plantation acreage in the country. Although it started the Oil Palm Development Programme in the early 1990s, growth was initially sluggish in the sector.

In 2014, the federal government launched the National Mission on Oilseeds and Oil Palm (NMOOP), with a special emphasis on expanding palm oil plantations in watersheds and wastelands. The agriculture ministry said at that time that India has the potential to grow plantations in nearly 2 million ha of land.

NMOOP started promoting plantations in 13 states, with financial incentives given to planters to buy plants and maintain them for four years. As a result, oil palm plantations grew from 8,585 ha in 1991-92 to 316,600 ha in 2016-17, official data show.

Despite the efforts, production reached just a quarter million tonnes in 2017-18 against domestic demand of over 10 million tonnes. Currently, a number of large Indian companies including ITC, Godrej Agrovet, and Ruchi Soya, are engaged in oil palm cultivation in India. Many of their plantations are in collaboration with provincial governments, particularly in the southern states of Andhra Pradesh, Telengana, Karnataka and Tamil Nadu.

To allay fears of deforestation, domestic palm oil producers say production in India is focussed in coastal states like Telangana and Andhra Pradesh, where expansion is taking place in already degraded land or in areas that were until then being used for water-hungry cash crops like cotton and paddy.

NMOOP’s latest target was to bring an additional 105,000 ha under oil palm cultivation by the year ending March 2020, bringing total area under cultivation to 420,000 ha. Official figures on achieving this target have not been released yet.

Import dynamics

It is now clear that, in the face of rising demand, domestic production will remain way under 10% in the years to come. That essentially means that India will continue to import palm oil in various forms. However, the dynamics of imports is not just dictated by demand but also geopolitical reasons. For instance, diplomatic tensions with Malaysia led the Indian government to discourage imports of refined palm oil for the Southeast Asian nation, resulting in a precipitous fall in recent months.

Domestic palm oil processors, such as millers and refiners, also routinely demand restrictions on imports so they can protect their margins. SEAI has recently presented the government with a list of demands that would favour local processors. This puts further price pressures in Malaysia and Indonesia, making it more difficult to green the palm oil supply chain.

The cost of ethical palm oil

Consumption patterns of edible oils in India depend on the category of users, with mass market commercial establishments preferring palm to more expensive alternatives like sunflower and soybean oils, as do lower income groups with limited spending power. Higher-income groups typically opt for other oils generally perceived as healthier, like sunflower or rice bran oil.

There is also a huge market for blended oils, a mix of palm and vegetable oils. Often, blended oils do not indicate the presence of palm oil in product packaging.

$30

The premium in the domestic market for certified sustainable palm oil (per tonne of crude palm oil)

Such factors often deter companies from making sustainability efforts. But the main factor appears to be price.

The premium in the domestic market for certified sustainable palm oil is around US$30 per tonne of crude oil, according to Palm Lines, a report on the industry in India.

The refined vegetable oil sector, by far the largest market segment, deals on high volumes and narrow margins. This segment often sells unbranded cooking oils to commercial or low-income buyers. Here the cost implications of even a small increase are significant.

According to industry executives, the competition to offer cheap products is so high that most companies will have no margins left if they were to add the costs of ethical palm oil. There are, however, some glimmers of hope. Some big refiners are moving away from so-called loose oil to actively marketing packaged and branded oils, where margins are higher and customer expectations differ. Although currently health is the defining characteristic of advertising campaigns, sustainability factors could possibly find a place in this higher-end bracket of the cooking oil market in the future.

Path to sustainability

Realising the importance of the Indian market to drive sustainability efforts in the global palm oil sector, the India chapter of the Roundtable on Sustainable Palm Oil (RSPO), which sets benchmarks for certified sustainable palm oil (CSPO), has become active in the country in the past few years in collaboration with the Centre for Responsible Business, Rainforest Alliance and WWF India.

In October 2018, these organisations launched the Sustainable Palm Oil Coalition for India (I-SPOC) to promote the sustainable consumption and trade of palm oil along the supply chain through industry collaboration. It has since set up working groups on government policy, supply chains and end users.

Ultimately, better consumer awareness on the effect of unsustainable palm oil to the world’s remaining rainforests is required

RSPO India officials say the initial signs have been encouraging, mainly with multinational corporations that have made global commitments to use CSPO. However, that comprises a small fraction of the Indian market and currently less than 5% of products that include palm oil fall under the umbrella of CSPO.

RSPO is working with stakeholders in India’s palm oil sector to lobby the government for policy responses that would encourage the use of CSPO. Progress on this front has been slow, mainly due to cost factors in a price-sensitive market.

To get around price issues, there are suggestions to adopt low-costs approaches to sustainability such as Sustainability Policy Transparency Toolkit (Spott), a free, online platform supporting sustainable commodity production and trade developed by the Zoological Society of London in 2014. WWF India says the Spott approach offers a flexible interim solution to large volume palm oil buyers without placing significant upfront cost on low-margin Indian businesses.

RSPO has also opened up another front in sensitising India’s smallholder plantation owners on sustainable practices. This initiative was to be launched in April this year but has been delayed due to the coronavirus crisis.

Efforts have also started to increase the physical volumes of CSPO in the market. Large Indian companies such as Adani Wilmar, Ruchi Soya and Godrej Agrovet have made commitments to CSPO, but there are not yet any targets. Ultimately, better consumer awareness on the effect of unsustainable production and processing of palm oil to the world’s remaining rainforests is required to drive companies dealing with the commodity to shift to CSPO. RSPO India has started another initiative to engage with the youth in India to raise such awareness but it’s a small beginning and there is much ground to cover for it to make a material difference.

This article is part of our ongoing series on palm oil. Click here to explore the series so far.

![A resident of Tetelisara village in Assam’s Nagaon district carries out his foodgrain stock during Assa, floods Nagaon May 2020 [image by: Diganta Talukdar/Alamy]](https://dialogue.earth/content/uploads/2020/06/Assam-floods-300x200.jpg)

![Tourists on elephants take photos of rhinos in Kaziranga National Park [image by: Sadiq Naqvi]](https://dialogue.earth/content/uploads/2020/06/tourists-on-elephants-take-photos-of-rhinos-in-kaziranga-file-photo-Nov-2019-300x225.jpeg)