Latin America is facing three perilous crises. The region is now the epicentre of the Covid-19 pandemic and is projected to have the worst economic performance in the world. As if these two crises weren’t enough, their combined impact threatens to worsen ongoing environmental devastation, especially in the Amazon basin. Though China is a relatively smaller part of the problem, it should be part of the solution.

2020’s triple crisis and the urgent need for debt relief

If Latin America sneezes when the US catches a cold, what happens when the world struggles with a global pandemic?

6

of the 10 countries worst hit by Covid-19 are in Latin America and the Caribbean

Latin America and the Caribbean (LAC) has been more affected by Covid-19 than anywhere else. As of this writing, six of the 10 worst-hit countries – measured in the share of the population that has succumbed to the virus in the last week – are in the LAC region: Peru, Bolivia, Brazil, Colombia, Chile, and Mexico. Four more are in the hardest hit 20 countries: Guatemala, Argentina, Ecuador, and the Dominican Republic.

The resulting economic pain is hard to overstate. The IMF now expects the region to experience the worst economic performance in the world this year, projecting economic decline of 9% and a drop as severe as 10% in Mexico. While LAC governments are trying to see their economies through this painful year, they are also facing ballooning debt service payments – even if they don’t take on new debt.

The reason for this is simple: most LAC countries cannot borrow in their own currency. Their debt levels depend on the value of the dollar. When investors sense instability and “retreat to safety” by selling off holdings of LAC currency, dollars get more expensive. This also applies to existing dollar-denominated debt, which can skyrocket as a share of LAC countries’ local economies.

These two crises exacerbate ongoing environmental problems, particularly burning in the Amazon basin. This year is expected to bring record or near-record fires in the world’s largest rainforest. Last month saw the highest number of fires for any June in the Brazilian Amazon since 2007. Furthermore, dry weather patterns in Western and Southern Amazon-basin countries Peru and Bolivia are setting the stage for “widespread” fires there too.

If China acted bilaterally it could require borrowing nations to spend the relief funds to attack the virus and embark on a recovery that is both socially inclusive and low carbon

The fact that these conditions are coming during a year of economic crisis, when governments are facing painful fiscal cuts to stave off debt crises, raises the spectre of slashed enforcement budgets that can’t cope with the rate of environmental damage. To make matters worse, smoke from Amazon fires is expected to exacerbate the Covid-19 toll in the already hard-hit region. Alleviating the debt burden is a crucial part of managing not only the economic crisis, but also the simultaneous health and environmental crises.

Longer term, the pandemic and ensuing economic crisis jeopardise the region’s plans for climate change mitigation and adaptation. Debt relief – whether multilateral, bilateral, or with bondholders – is a crucial element in safeguarding the region’s climate fight. For example, green energy projects tend to cost more to install, but cost less in the long term. So, a short-term economic crisis can make those investments harder to justify even as they become more necessary in the long-term.

More than anything, LAC needs the fiscal (or budgetary) space to effectively manage the virus and mount a comprehensive recovery. Unfortunately, fiscal space is tight because of the large amount of dollar-denominated debt countries owe their creditors. While debt relief initiatives have begun on three fronts – multilateral, bilateral, and with bondholders – progress has faltered and has not offered LAC much respite.

China can play an important leadership role in bringing much-needed help to the region.

Multilateral liquidity and debt relief

In the multilateral arena, a new issuance of IMF Special Drawing Rights (SDRs are the IMF’s unit of account that can be used to pay other Central Banks and certain international institutions) would really help. As would significant debt relief from private and bilateral creditors. Unfortunately, the US and private creditors have blocked efforts on SDRs and broader debt relief to lower and middle income countries – the category that includes most Latin American countries – and the private sector.

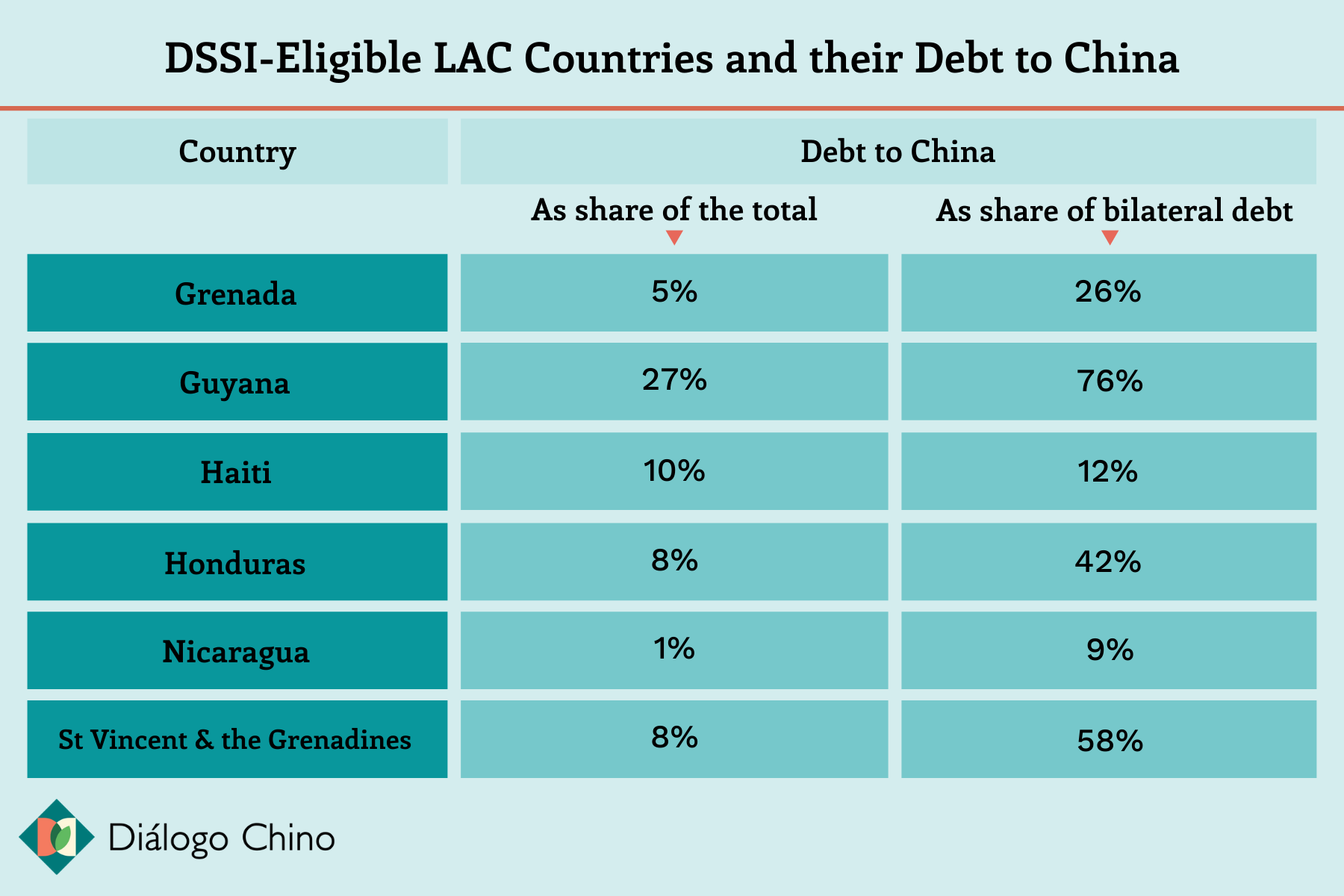

The G20 has taken a small step in the right direction by establishing the Debt Service Suspension Initiative (DSSI) that would provide a suspension of debt payments for the rest of the year to approximately 73 of the world’s poorest countries. Unfortunately, most LAC countries are middle-income and do not qualify for DSSI.

Bilateral debt relief

There is a tendency to point to China as the source of the problem. China is part of the problem but to focus solely on China misses the point. There are some countries whose debt to China stands out, but if private bondholders don’t participate in debt relief too then any action by China would serve to benefit them, rather than Latin American people and their economies.

Just six LAC countries are eligible to participate in G20s DSSI. Among them, only two – Guyana and St. Vincent and the Grenadines – owe the majority of their bilateral debt to China.

Bilateral debt relief – from China or from other creditors – can be a crucial help, but it also comes at a cost. Sovereign credit rating agencies downgrade countries that participate in debt relief, which can cause even greater economic pain. It should come as no surprise that of these six countries, only one – Guyana – has participated.

However, even by participating in the DSSI, Guyana will not necessarily receive debt relief from China. According to the Financial Times, China Development Bank is not considered an official bilateral creditor. As such, it will not participate in the DSSI. There is no publicly-available information as of this writing about whether the China Export-Import Bank (Guyana’s most important Chinese creditor) will participate. As national development and policy banks, they should join this effort, together with their peers the KfW (in Germany) and JICA and JBIC (in Japan).

Guyana, Ecuador, Jamaica and Venezuela, have a large exposure to China. China is a greater part of their general external debt and their largest bilateral official creditor.

The biggest problem for the region, which the G20 has thus far failed to rein in, is the private sector. The table below shows that official bilateral debt is only 6% of total outstanding debt (with China the largest bilateral debtor in that category). The bulk is held by private bondholders and commercial banks. This is largely due to corporate sector bond issuances in Latin America and foreign investors in the West, and fuelled by low interest rates in the US and quantitative easing in the wake of the 2008-9 financial crises.

Latin America is already feeling the impacts of a weak G20 as creditors repeatedly reject good faith restructuring proposals from Argentina and Ecuador. This has led China and other creditors to rightly pointed out that it would be unfair for China to provide debt relief only for borrower countries to then use those funds to pay private bondholders in the West. The funds should be used to manage the health crisis and mount a sustainable recovery.

How China can help

To China’s credit, it pressured the IMF and G20 to expand IMF Special Drawing Rights in April and again last week in the IMF. This move would have brought immediate relief to many Latin American countries, not just the poorest. Unfortunately, the US and India blocked that effort.

Latin America needs SDRS and debt relief from bilateral creditors and, above all, from the private sector. Without that effort, no foreign actor has an incentive to participate. This will require multilateralism. But time is running out and China has little influence in the G20 and IMF.

If China acted bilaterally it could require borrowing nations to spend the relief funds to attack the virus and embark on a recovery that is both socially inclusive and low carbon. China’s leadership could make others follow.

![Residents of Thakurbari place sand-filled bags on the Koshi riverbank in an effort to save the riverbank and their homes from floodwaters [Image by: Birat Anupam]](https://dialogue.earth/content/uploads/2020/08/Nepal_Floods_2020_Koshi_1-300x199.jpg)